Nearly half of VCM projects are deemed ‘low integrity’

MSCI finds no top-tier projects despite research suggesting 40% of firms plan to use offsets to achieve climate goals

Almost half the world’s carbon-credit projects are “low integrity,” according to a major study published today.

Data and finance giant MSCI assessed more than 4,000 projects on factors such as how long they can guarantee emissions reductions, and whether those reductions would happen without the voluntary carbon markets providing a source of funding.

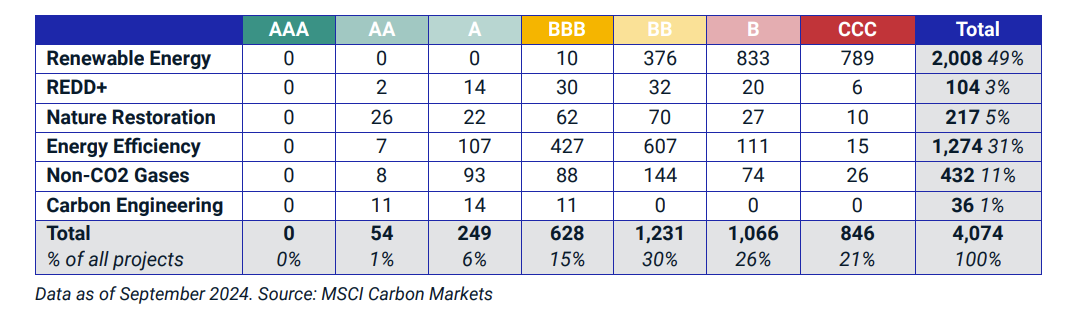

Each project was awarded a score between AAA and CCC.

AAA-labelled projects are those believed to have “a very high likelihood” of delivering “at least a 1 tonne CO2e emissions-impact per credit, and a range of positive social and/or environmental outcomes while upholding legal and ethical standards”.

CCC, on the other hand, relates to projects with “significant risks regarding either delivering a 1 tonne CO2e emissions-impact per credit or supporting material positive social and/or environmental outcomes while upholding legal and ethical standards”.

While no projects secured a AAA rating, 47% were labelled as either CCC or the band above: B.

Grid-connected renewables were generally seen as the least able to demonstrate additionality, meaning they would probably have existed anyway, without the need for carbon credits.

In contrast, projects that remove carbon from the atmosphere are typically very dependent on the revenues generated by carbon credits to survive.

In terms of permanence – the length of time a project is likely to be able to save or store carbon – cookstoves ranked poorly, while carbon-engineering projects scored well.

The evaluation is based on a framework developed in 2021 by well-known research house Trove, which MSCI acquired last year.

Other areas assessed include whether the projects have broader environmental and social benefits, how risky they are, and whether they pose ethical issues.

Pricing

MSCI found that projects with higher integrity scores in the study “traded at a clear and statistically significant premium to lower-integrity projects” over the past two years.

“After controlling for other factors, such as project type and location, a 1-point improvement in a credit’s overall integrity score (1-5) has been associated with an 8% increase in its spot price,” the firm said.

“A closer relationship between integrity and price in the future will likely support a better functioning carbon market, where incentives are more aligned toward supplying and choosing higher integrity credits.”

The future of offsets

Concerns about the integrity of carbon credits has led some companies to back away from the market in recent years.

In 2023, more than half of respondents to a survey by the Science Based Targets initiative said they had been put off buying any more carbon credits because of worries about being accused of greenwashing.

Despite the cooling, though, offsetting specialist Climate Impact Partners reported last week that more than 40% of major firms “explicitly state they will use carbon credits to meet a carbon neutral or net zero target”.

MSCI said that were signs the credibility of the voluntary markets was improving, in part due to efforts to strengthen governance and oversight, and because the biggest offsetting registries had upgraded their methodologies, transparency measures, governance and grievance mechanisms.

“There are some early signs of a trend to increasing integrity,” the report claimed. “First, there has been a gradual shift in retired credits moving toward higher-integrity projects. Second, new projects being developed also appear to be, on average, of higher integrity.”

Regulation

The European Roundtable on Climate Change and Sustainable Transition warned EU lawmakers last week that its approach to clamping down on greenwashing may have unintended consequences for the voluntary carbon markets.

In a report about the proposed Green Claims Directive, the Brussels-based think tank said that, while the law “is presented as intending to ensure consumer protection and fair competition, and not to regulate (voluntary) carbon markets”, it ends up doing the latter.

“When purportedly voluntary initiatives become subject to an increasingly dense regulatory fabric, it adds to existing concerns about the burden of overregulation and enforced protectionism that alternatively contributes to the dense regulatory puzzle facing companies operating in Europe and the decreased levels of innovation and competitiveness currently diagnosed in the EU,” the report stated.